The Hong Kong Monetary Authority (HKMA) has released a technical whitepaper on a retail central bank digital currency (CBDC), proposing an architecture that would follow the key principles of safety, efficiency, and openness.

The paper, titled e-HKD: A technical perspective, shares findings from a technology experimentation study, exploring potential architectures and design options for issuing and distributing a retail CBDC, and proposing a possible design for what is believed to be the ideal retail CBDC system.

The HKMA’s proposed retail CBDC infrastructure

The CBDC architecture would consist of two layers: a wholesale system for the central bank to issue and redeem the digital currency, and a retail system for commercial banks to distribute and circulate either retail CBDC or CBDC-backed e-money.

The wholesale CBDC issuance and redemption system would only be accessible to intermediaries such as commercial banks and payment service providers (PSPs) as well as the central bank, while the retail CBDC/e-money distribution and circulation system would only be accessible by intermediaries and users in the general public equipped with mobile wallet applications.

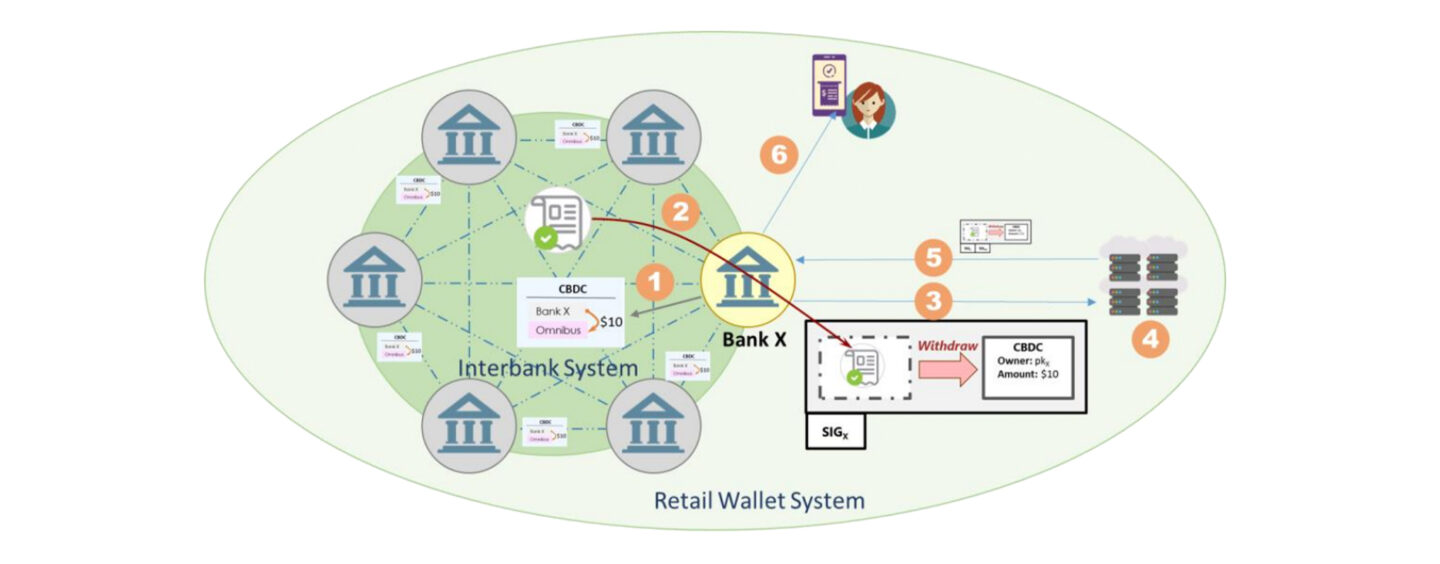

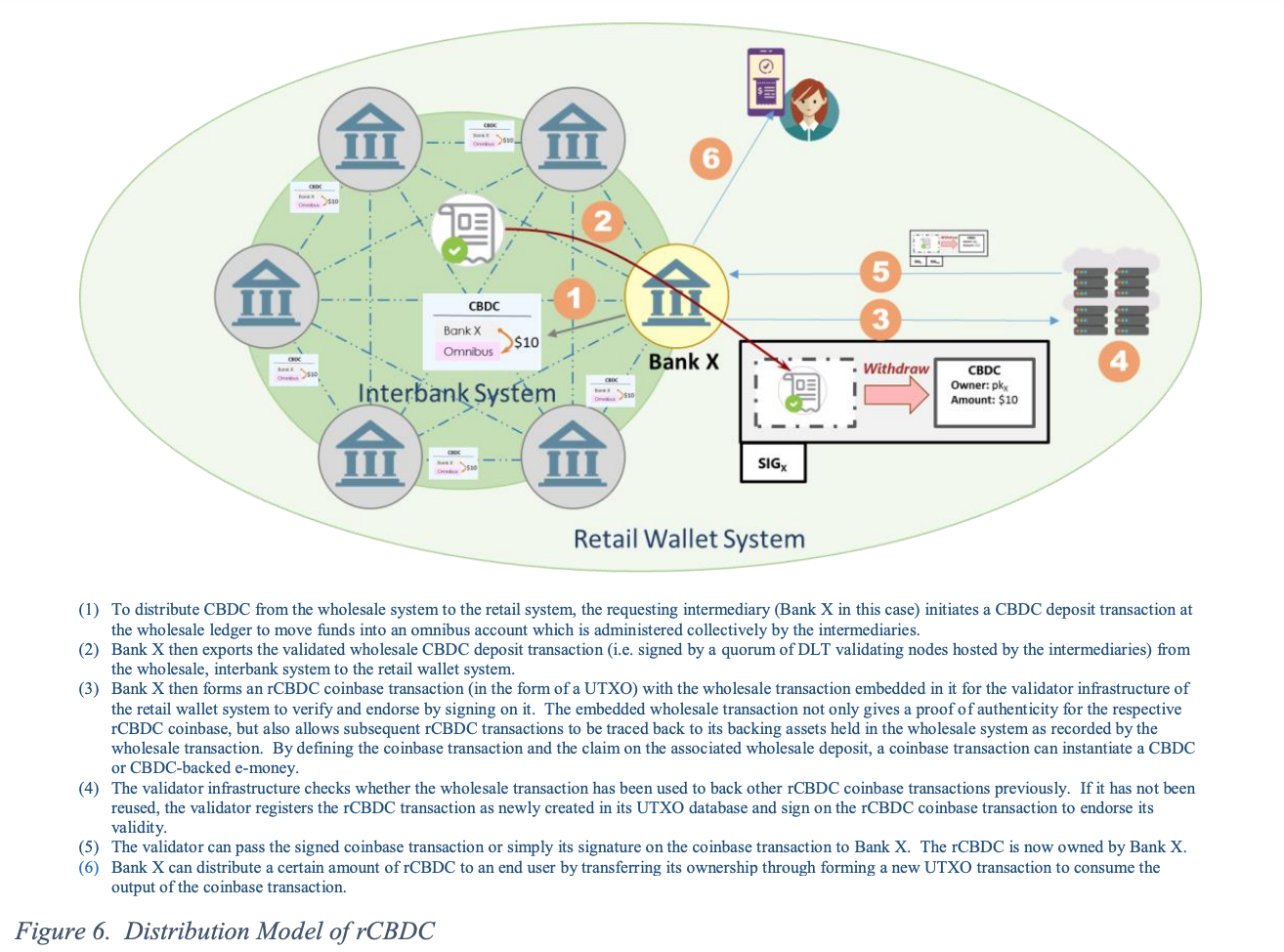

Distribution Model of retail CBDC, Source: e-HKD: A technical perspective, Hong Kong Monetary Authority/Bank for International Settlements Innovation Hub Hong Kong Centre

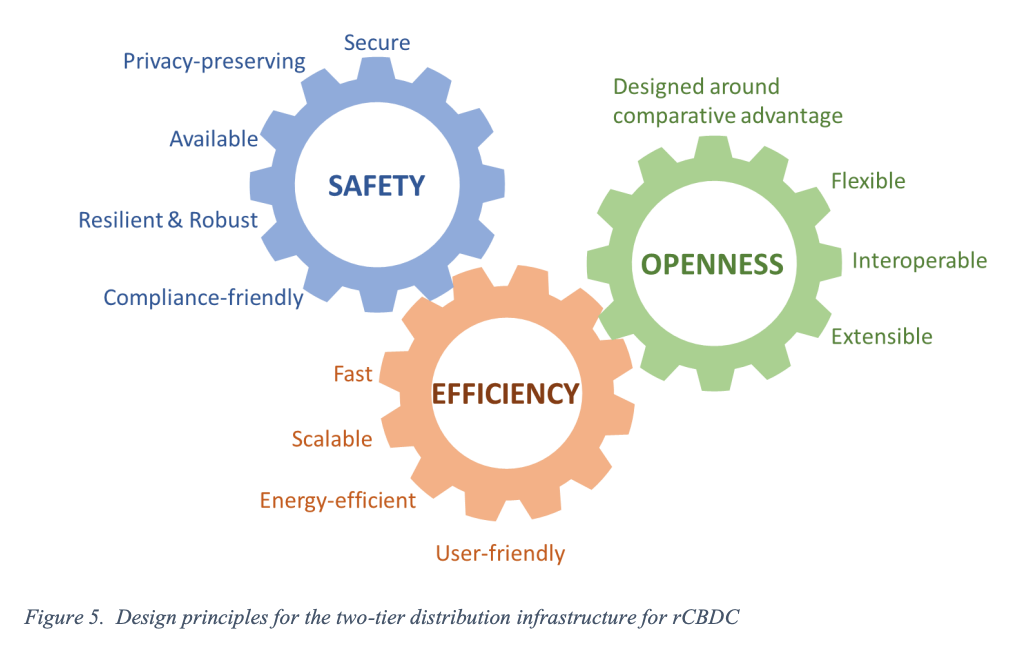

This system should be designed following several key principles. These include safety, where a CBDC, as a payment system, should perform reliably at all times, be secure, resilient and robust, as well as compliance-friendly. The system should also be privacy-preserving where only necessary data are disclosed to relevant parties as needed for processing transactions and fulfilling relevant compliance requirements.

The retail CBDC system must be efficient in regards to speed, scalability and energy. It should be user-friendly, intuitive to the typical user as well as accessible for the widest group of users, including those who are physically challenged and those who face barriers in access to hardware or data networks.

Openness is another key principle where the CBDC system, as a whole, should remain open to change, innovation and competition. The system should be able to evolve with the changing needs of users and central banks, interoperable with other countries’ CBDC payment systems, and extensible in the sense that it should include sufficient room for future enhancements or extensions.

Design principles for the two-tier distribution infrastructure for retail CBDC, Source: e-HKD: A technical perspective, Hong Kong Monetary Authority/Bank for International Settlements Innovation Hub Hong Kong Centre

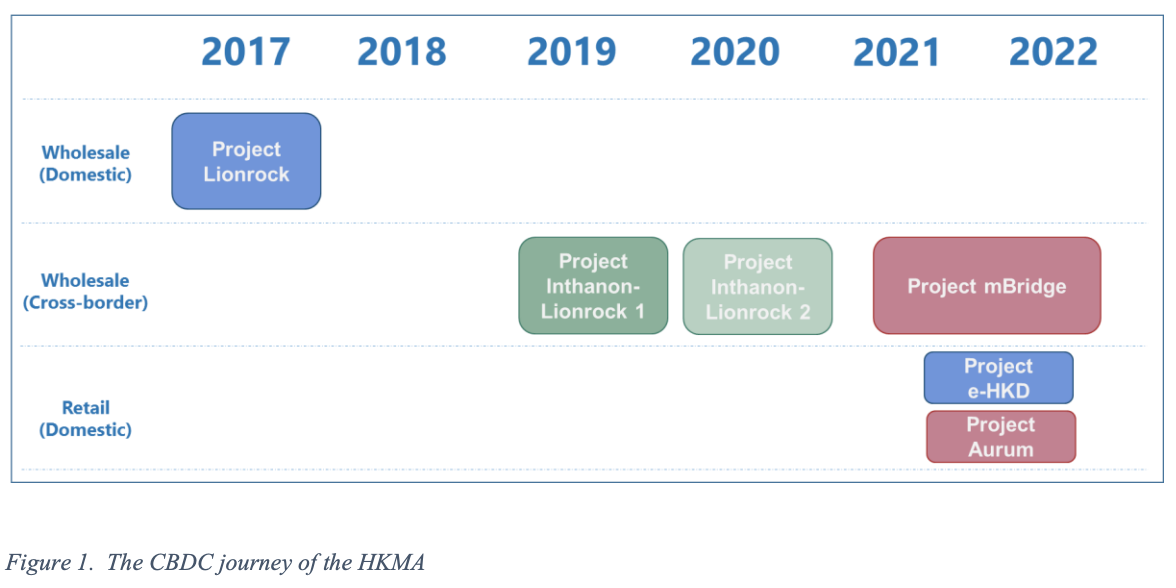

The HKMA’s digital currency journey

The HKMA began researching CBDC in 2017 under Project LionRock. The project initially sought to better understand the feasibility, implications and possible benefits of a digital currency, and later evolved into exploring the potential of a CBDC at the wholesale level.

This developed into a collaboration with the Bank of Thailand to study the application of a CBDC to cross-border payments. Project Inthanon-LionRock was completed in December 2019 and a distributed ledger technology (DLT)-based proof-of-concept (PoC) prototype was developed together with ten participating banks in both jurisdictions.

Upon completion of Project Inthanon-LionRock, the HKMA’s CBDC research project entered its next phase and was renamed to Project mBridge (Multiple CBDC Bridge) in 2021, adding the Central Bank of the United Arab Emirates and the Digital Currency Institute of the People’s Bank of China (PBoC) into the initiative.

Project mBridge, which now counts four central banks and which is being supported by the Bank for International Settlements (BIS) Innovation Hub Centre in Hong Kong, is exploring the use of DLT to enhance the financial infrastructure for cross-border payments.

In parallel, the HKMA kickstarted in mid-2021 Project e-HKD, which focuses on retail CBDC and explores the potential of issuing a digital version of the Hong Kong dollar, as well as Project Aurum, which studies the technical feasibility and trade-offs of intermediated CBDC and CBDC-backed e-money.

The CBDC journey of the HKMA, Source: e-HKD: A technical perspective, Hong Kong Monetary Authority/Bank for International Settlements Innovation Hub Hong Kong Centre