South Koreans are increasingly going cashless as more people turn to e-wallets in South Korea for both online and offline purchases.

Figures can attest of the rapidly growing trend with 2.12 million won (US$1,800) worth of mobile payment transactions being made daily in 2017, up by a staggering 147.4% on-year, according to the 2017 Electronic Pay Service Usage report released last year. The total volume of payments facilitated by simplified mobile payment services reaching a record 67.2 billion won (US$57 million), up 158.4% from 2016.

South Korea’s mobile payment and e-wallet players

To tap into this growing opportunity, tech firms, credit card companies and even the government have launched varied mobile payment services.

Samsung Pay is undeniably one of the leading mobile payment systems in South Korea. Samsung Pay, which the smartphone manufacturer launched in 2015, is a mobile payment and digital wallet service that uses near field communication (NFC) and magnetic secure transmission technologies to allow users to make contactless payments using compatible phones by linking a debit or credit card.

Samsung Pay, Samsung

The total transaction volume of Samsung Pay had exceeded 40 trillion won (US$33.68 billion) at the end of April with the number of subscribers surpassing 14 million, reports Business Korea. In 2018, the service accounted for 80% of the offline simple payment market in South Korea, according to the Financial Supervisory Service.

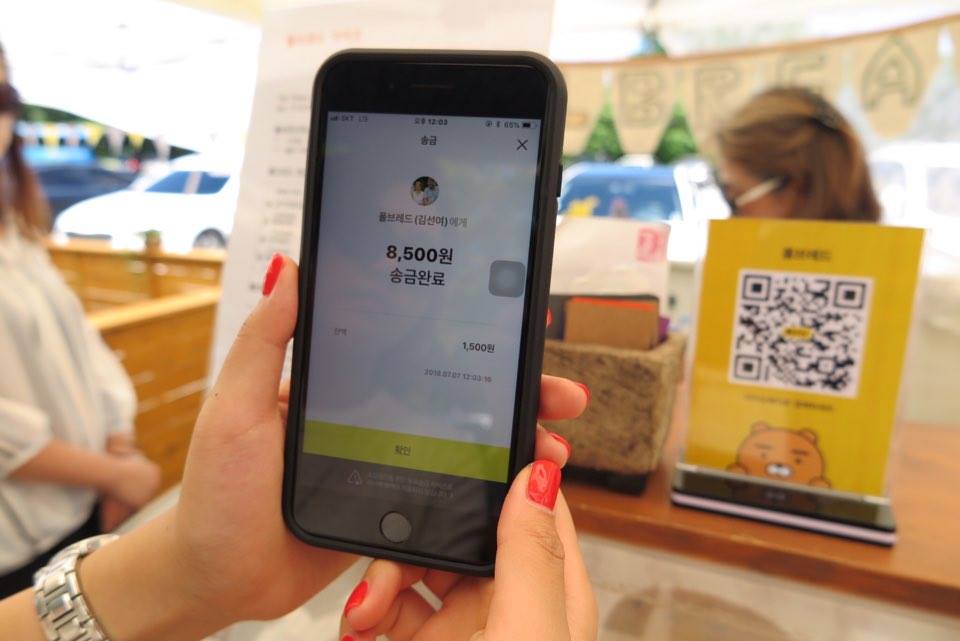

Among the early pioneers of mobile payments in South Korea, Kakao, the operator of South Korea’s number one messaging app KakaoTalk, launched Kakao Pay in 2014 to allow users to make online transactions and mobile payments using NFC and QR codes.

Since its release, Kakao has expanded into other financial services by releasing for instance its own debit car and launching its own bank (Kakao Bank) and investment service (Kakao Investment). Kakao Pay has also added more features like the ability to send remittances, send invoices, and complete online transactions on mobile, with an aim to become an “integrated financial platform.”

Kakao Pay crossed the 10 million user mark 20 months after being released and transactions made using the service exceeded 2.3 trillion won (US$2.04 billion) monthly, as of October 2018.

With the rapid increase in users and transactions, Kakao Pay received a US$200 million investment from Alibaba’s Ant Financial in 2017.

Naver, South Korea’s leading web portal and search engine, launched Naver Pay in 2015. Naver Pay is a mobile payment service that allows both mobile payments through the app and online checkouts for online shopping similar to PayPal. As of October 2018, the total number of Naver Pay users exceeded 26 million and the industry estimated its monthly average transaction amount to be around 900 billion won (US$797.17 million).

Naver Pay is the firm’s second mobile payment service after Line Pay, an e-wallet integrated into the Line messaging platform, the top messaging app in Japan. Line Pay allows users to request and send money from users in their contact list and make mobile payments in store. Since its introduction in 2014, the service has expanded to allow other features such as offline wire transfers when making purchases and ATM transactions like depositing and withdrawing money. Like Kakao Pay, Naver Pay seeks to establish an ecosystem.

QR code payments on the rise

QR code payments, though still nascent, are rapidly growing in South Korea with Kakao QR Pay recording 190,000 partner stores and 3 trillion won (US$2.562 billion) worth of transactions as of December 2018.

Kakao Pay, kakaopay, Facebook

In late 2018, three South Korean credit card companies, namely BC Card, Shinhan Card and Lotte Card, unveiled plans to commercialize a solution called Joint QR Pay that would be compatible at 8 million franchise stores in South Korea. What makes this solution different is that payment requests would be accumulated and paid in full on the monthly due date, similar to how credit cards work.

The South Korean government itself launched in March a mobile payment system called Zero Pay. Initiated by the city of Seoul and the Ministry of Small and Medium-Sized Enterprises (SMEs) and Startups in partnership with local banks and finance companies, Zero Pay is a mobile payment system that allows users to make payments by scanning a vendor’s QR code.

Zero Pay can be accessed through the mobile apps of major banks, including KB Kookmin Bank and Woori Bank, as well as Bank Pay, a multifunctional app that links to 19 local banks.

Favorable regulations

As South Korea’s digital payments market heats up, the country’s Financial Services Commission (FSC)’s decision to open the closed inter-bank payment networks to non-bank financial companies will likely see the market get even more crowded.

The move would allow domestic banks and fintech companies to freely access the payment networks set up by other banks, and enable them to more easily create innovation financial products and services.

The FSC is also planning to establish an open banking system by the end of this year and will revise the Electronic Financial Transaction Act.

Image Credit: Edited from Freepik here and here