Chinese Fintech Attracted Investments of Over US$ 900 Million in 2H 2019

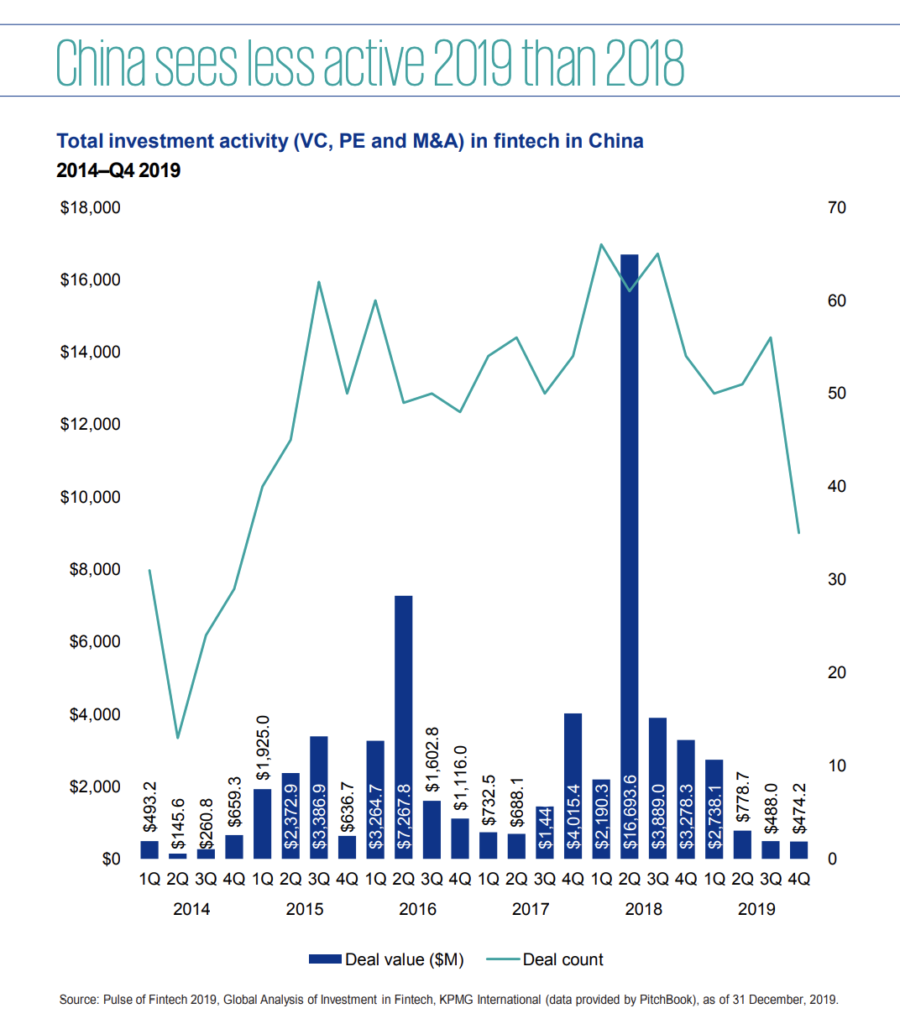

by Fintech News Hong Kong March 2, 2020Fintech companies in China attracted USD 962.2 million in investments from venture capital, private equity and M&A in 2H 2019, resulting in a total of USD 4,479 million in investments for the whole of 2019, according to KPMG’s Pulse of Fintech H2’19 bi-annual report on global fintech investment trends.

Fintech investment in China took a breather after a massive 2018, but the country’s fintech market continued to see substantial activity and Chinese companies still ranked among the largest fintech deals in Asia Pacific for the whole of 2019.

China’s large technology giants continued to focus on growing their reach geographically, making investments or plays well outside of Greater China. Ant Financial, for example, submitted an application for a digital banking license in Singapore in late 2019, while Tencent made a number of significant investments in fintech companies in other regions throughout the year, including Ualá in Argentina.

Investors in China also began to turn their attention to up-and-coming areas of fintech. These include regtech, which has appeal among VC investors because of its ability to leverage artificial intelligence and machine learning to assess risk and identify fraud.

China-based investors are also interested in fintech companies that use these technologies more broadly to improve the operations of banks and financial institutions, such as improving operational efficiencies, generate and analyse data, as well as support wealth management.

The third quarter of 2019 saw the People’s Bank of China unveiled a three-year plan to support the development of the fintech industry. Since then, there has already been a number of moves focused on implementation. For example, a fintech sandbox is in development, with testing currently being concluded in Beijing. It is expected that this plan will help fuel future investment in fintech, particularly in key areas like risk management, cybersecurity, big data, artificial intelligence, distributed databases and authentication.

Chris Wang

Chris Wang, Partner, Head of Fintech, KPMG China, commented,

“China’s central bank and other authority bodies are working to move fintech in the country to ‘2nd half’ as part of their three-year fintech development plan. We anticipate an increased regulation and guidance for the industry and an enhanced infrastructure to support fintech development. For example, sandbox mechanism is being designed and may soon roll out to test the concept of different fintech to make sure they comply with regulations and will achieve the desired results before they enter the market.”

The fintech market in Hong Kong saw some resilience in the fourth quarter of 2019, particularly on the back of Alibaba’s decision to do a secondary listing on the Hong Kong Stock Exchange, which raised USD 11.2 billion, making it the largest listing of the year globally.

Earlier in 2019, Hong Kong issued the first batch of eight digital banking licenses. ZhongAn was the first to launch a digital bank pilot, with others expected to follow suit in 2020. As the licensees continue to formulate their digital bank offerings, Hong Kong could see an upswing in investments in related areas, like KYC, regtech, digital onboarding and communications, and digital banking infrastructure. The issuance of digital banking licences has also spurred traditional banks to improve their own digital offerings and experience.

Avril Rae

Avril Rae, Director, Head of Fintech, Hong Kong, KPMG China, said,

“We’re starting to see ecosystems evolving with respect to digital banks. Partners are coming together to get digital banking licenses. Once they have their pilot projects underway, and they have proven their technology both internally and to the Hong Kong Monetary Authority, we’ll start to see them leveraging those partnerships more deeply – integrating banking services with other offerings like travel bookings or insurance to provide their customers with a seamless experience.”

Featured image credit: Unsplash